Clinical Trial Prediction Markets: Forecasting Evidence or Distorting It?

This is a topic that I had given no thought to before Dr. Windisch submitted this essay. I think I am less pessimistic about these markets than Dr. Windisch, maybe because I am more pessimistic about a lot of trials, but I certainly appreciate being introduced to this issue.

Adam Cifu

Prediction markets such as Kalshi and Polymarket have become commercially successful by allowing users to trade on the outcomes of real-world events, including elections, court decisions, economic data releases, sports results, and policy questions. The premise is straightforward: When people put money behind their expectations, the market price can be interpreted as a real-time estimate of the probability of an event. This has given prediction markets a prominent role in political forecasting.

More recently, there have been efforts to build prediction markets for clinical trials, some of which have attracted attention on social media. Proponents argue that such markets could democratize biotech forecasting, make clinical-development risks more legible, and aggregate dispersed information more efficiently than isolated expert commentary. They also note that clinical trial “betting” already occurs indirectly through biotech equities and event-driven trading, and that a dedicated prediction market might simply make these judgments more explicit.

This framing is too optimistic.

Clinical development can be slow, expensive, and inefficient. There is certainly room for improvement. The FDA has, for example, explored “real-time trials” with the goal of accelerating decision making and reducing reliance on rigid, discrete trial phases. But real-time regulatory review is not the same as public real-time speculation. The former can be governed by protocols, confidentiality rules, prespecified monitoring plans, and regulatory accountability. The latter may alter the informational and ethical conditions under which the trial is conducted.

One reason prediction markets sometimes perform well is that they may reward private information. In politics, for example, someone may have information about local campaign activity, turnout, polling quality, or institutional dynamics that is not yet fully reflected in public commentary. Whether this is desirable is debatable. In clinical trials, it is more clearly problematic.

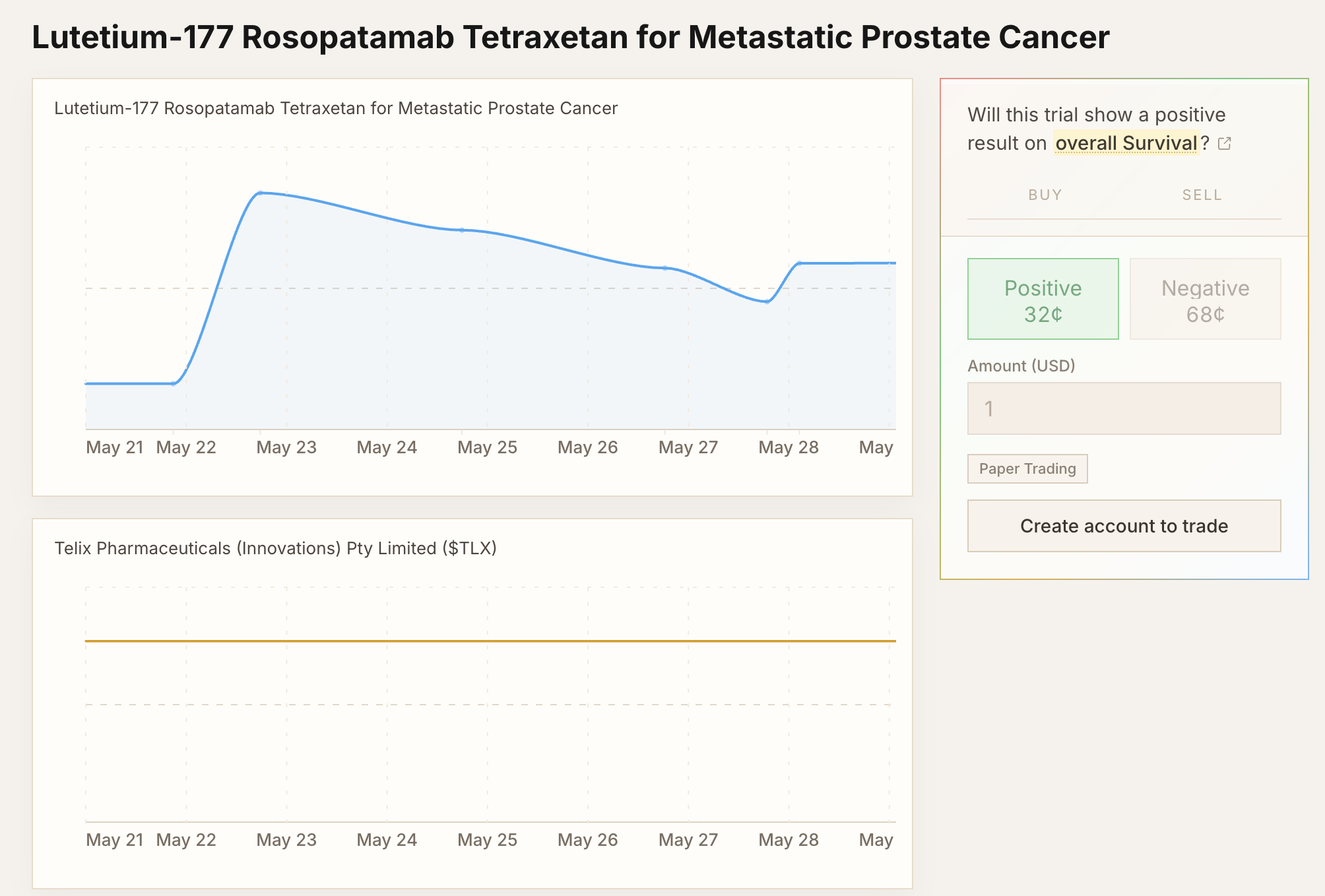

Consider a multicenter trial that has just started recruitment. One site has enrolled five patients. By chance, all five have had unfavorable outcomes: Early discontinuation, toxicity, or apparent lack of response. Even if the trial is blinded, staff at that center may form a negative impression. If someone with access to that local experience places negative predictions on the trial, the displayed odds may fall.

To an outside observer, those odds may appear to represent a global probability of trial success. In reality, they may reflect the early, incomplete, and potentially misleading experience of one site.

This matters because trial participation is sensitive to perceived benefit, perceived burden, and risk information. A patient considering enrollment may reasonably look for information about the trial online. If they find a prediction market showing unfavorable odds, they may decide not to participate. Physicians may also become less enthusiastic about referring patients. Recruitment may slow. Retention may be affected. In this way, the market could influence the outcome it claims only to forecast.

Clinical trial systems already recognize the risk that interim information can change conduct. FDA guidance on data monitoring committees notes that investigators who know early trends might alter recruitment or monitoring behavior, and it recommends that data monitoring committee members for a given trial not include investigators in that trial. The same guidance states that knowledge of unblinded interim comparisons can bias trial conduct or analysis, and that such data should generally be accessible only to the data monitoring committee or statisticians performing the interim analyses.

Prediction markets would create a public, tradable, continuously updated signal about an ongoing trial. This is difficult to reconcile with the principles that motivate restricted access to interim information.

The argument that insider trading already occurs through traditional financial instruments is only partly convincing. Traditional financial platforms usually have stricter know-your-customer requirements and more established surveillance mechanisms. In addition, the stock price of a larger biotech or pharmaceutical company is rarely determined by one trial alone. Other products, earnings, regulatory developments, and market-wide factors can all affect the share price. A trial-specific prediction contract is much more directly tied to one outcome.

Even if insider trading were not a concern, manipulation would remain a problem. An entity with a financial or strategic interest in a trial’s failure could place large negative bets, especially in a thin market, in order to move the displayed odds. Those odds could then deter enrollment or reduce confidence in the study. In this respect, clinical trials differ from many other events commonly traded on prediction markets. Elections, court decisions, and economic data releases may be forecast by markets, but the displayed odds are less likely to directly determine whether the event can be completed. Ongoing clinical trials are different. Publicly visible negative odds could become self-reinforcing.

Clinical development needs better forecasting, faster regulatory learning, and more transparent reporting. But public prediction markets for ongoing clinical trials are a poor solution to those problems. Trials are not passive events waiting to be predicted. They are systems whose validity depends on controlled information flows, participant trust, adequate recruitment, and sustained equipoise. Once trial-specific odds become public and tradable during recruitment, the market may no longer merely forecast the outcome. It may help produce it.

That risk, however, argues for regulation rather than a blanket rejection of the underlying technology. Sensible rules could preserve useful forms of forecasting while limiting the cases most likely to distort trial conduct. At a minimum, trial-specific betting should not be allowed while recruitment is still ongoing. Markets should also require know-your-customer procedures to reduce the risk that trial staff or others with access to non-public information trade on early, incomplete, or unblinded data.

Under such constraints, prediction markets may actually have a positive impact after recruitment is complete or after initial results are public. In oncology, for example, a market on whether an overall survival benefit will emerge after immature progression-free survival data have been reported could aggregate expert expectations about durability, clinical relevance, and downstream practice change without directly influencing patient enrollment. The goal should therefore not be to reject forecasting altogether, but to introduce sensible regulation so that it supports evidence interpretation rather than distorting evidence generation.

Paul Windisch, MD, is a researcher in radiation oncology at the Cantonal Hospital Winterthur in Switzerland, working on the implementation of artificial intelligence to structure information and to automate clinical workflows.

| A guest post by

|

Fear and greed drive the market. Don’t chase trends. Even in clinical trials/studies.

I couldn’t agree more with Dr. Windisch-medical studies leave much to be desired at the present time – adding prediction markets will only create further predictable and unpredictable issues – it will compound the confounders-

The financial markets were once defined as “perfect competition“. That means that everyone had the same information, and no one in theory had an advantage over someone else – that is laughable now, and the markets are closer to a casino– keep research, with all of it’s warts as highlighted at SM, at least

attempting to seek out the truth –

Ben Hourani MBA